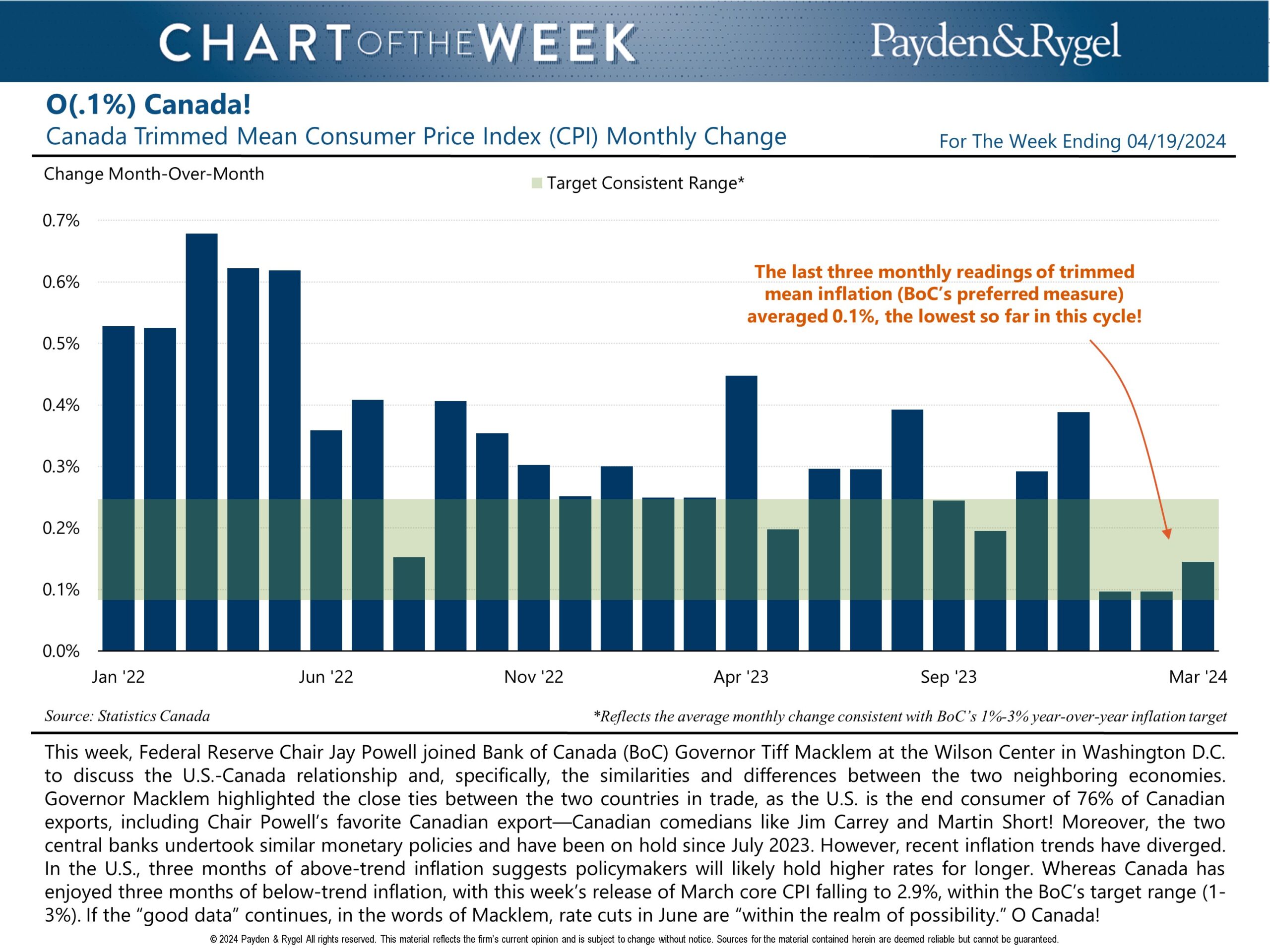

April 26

In the U.S., the yield on the US 2-year Treasury note remained stable at 4.62%. The yield on the benchmark 10-year Treasury fell to 4.20%, down from 4.25% at the end of February. The yield on the 30-year Treasury fell four basis points to 4.34%. In March, the US economy demonstrated its resilience, as inflation levels remained above those consistent with the central bank’s target and labor market demand continued to exceed supply.

Click here for most recent Market Commentary!

Funds professionally managed by Payden & Rygel for 29 years running.

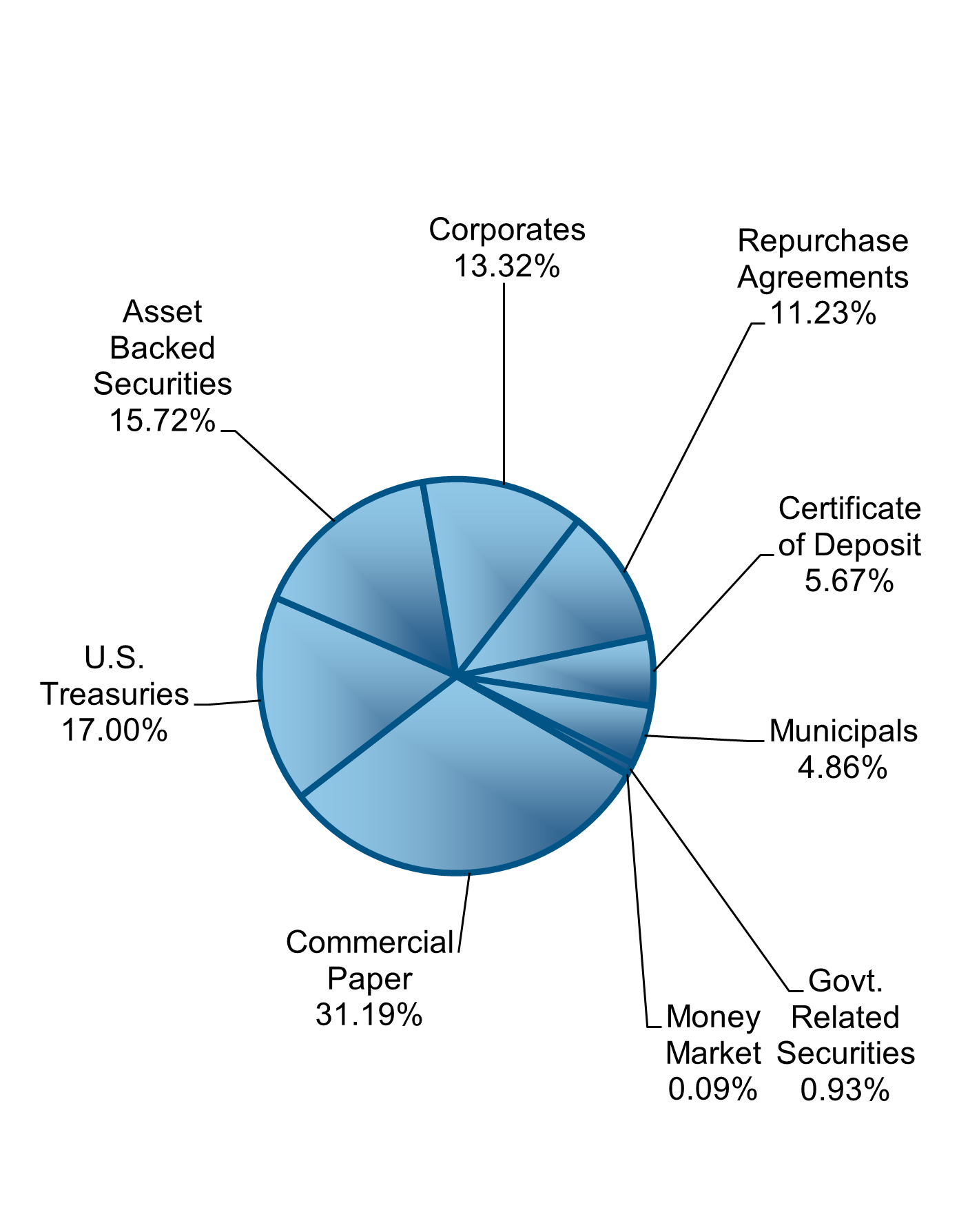

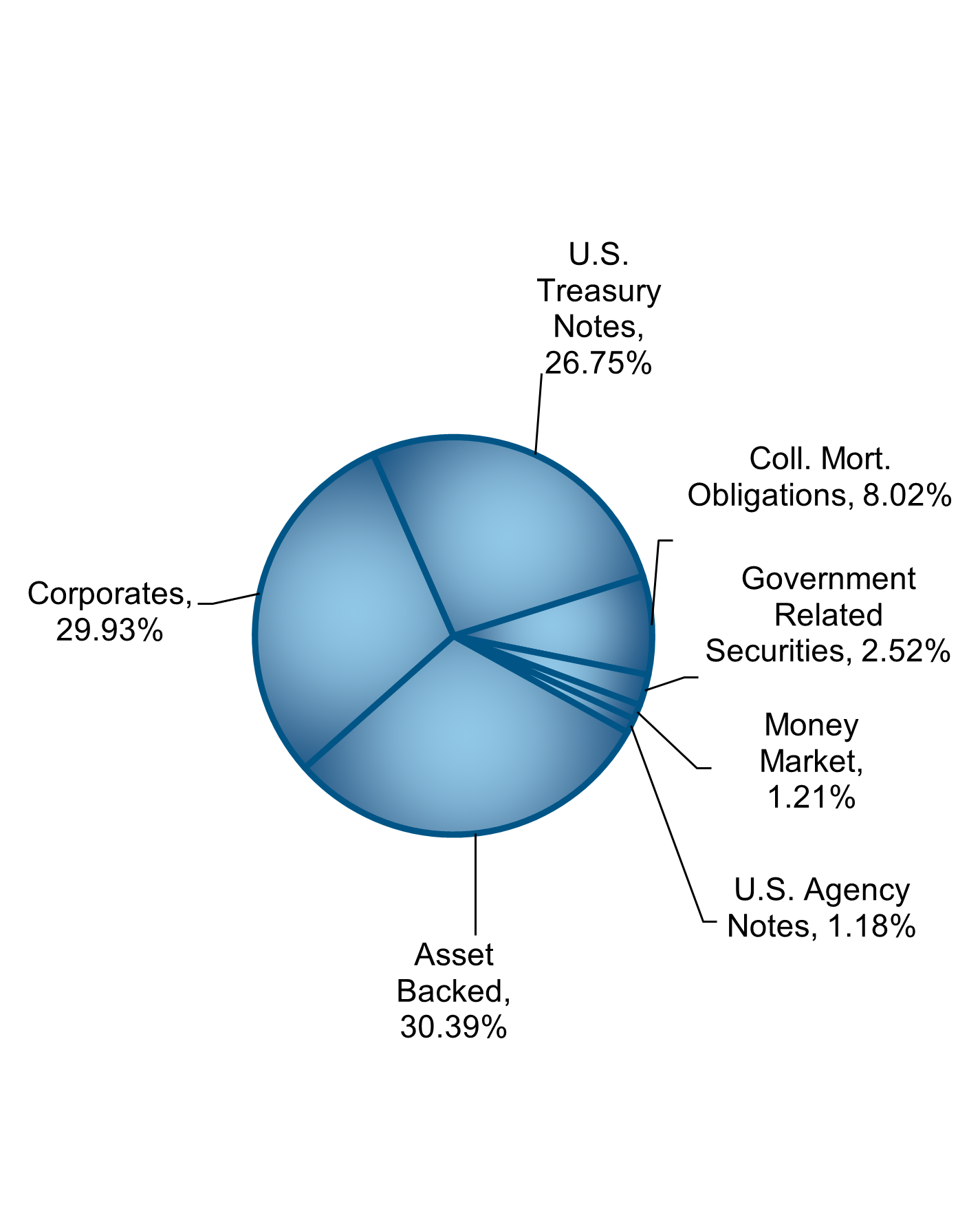

Sector Allocation

% of Portfolio Assets(03/31/2024)

Your Investment

How has your investment grown over time?